Estate Planning Explained: How to Leave Your Legacy

Estate planning can sometimes feel like a trip to the proctologist. You have some vague idea about why it’s needed, you typically put it off until its too late, and while you are doing it you think “how much longer is this going to take.” But estate planning should be a cornerstone of everyone’s life. More importantly, proper estate planning can save you money, time, taxes, and provide you with peace of mind. In this article, you will learn whether you like it or not, you will have an estate plan when you die. The only question is, do you want the State to make the plan for you, or do you want to control your own legacy?

Death and Taxes: Estate Planning in a Nutshell

In his 1789 letter to John-Baptiste Le Roy, Benjamin Franklin penned the often cited axiom “in this world nothing can be said to be certain, except death and taxes.” Every estate planner knows that this axiom is as true today as it was in 1789. The truth is, you will die. Unless you have a specific medical diagnosis, you likely do not know when, where, or how your life will end. But one thing is certain, it will end. When it does, every piece of real and personal property you own will need to go somewhere. Proper estate planning allows you to decide where your property goes when you die. It may seem like a complicated and daunting process, but it is not.

What is an Estate Plan?

Before we explain what “estate planning” is let’s first talk about what an “estate plan” is. An estate plan is an orderly process for determining what happens to your property when you die or are incapacitated. A good estate plan will also address who should make decisions for you in the event you are incapacitated and cannot make them for yourself. Everyone has an “estate plan.” No matter how rich or poor you are, there only three possible “plans” for your property on your death.

2. The Last Will and Testament plan.

I describe each of these “plans” in more depth in other articles. For now, there are only two words that you need to know to understand the differences between the three plans. Those words are: “probate” and “taxes.” The main differences between the three plans, above, are the extent to which they help you avoid probate and how they can help save your family from paying any estate taxes.

Why You Should Avoid Probate?

The word “probate” has the same Latin root as the English word “probe.” It simply means to test something or prove something. As its sister word “probe” indicates, probate can be a real pain in the butt.

A “probate” is the formal testing or proving of a will in a special court called a “probate court.” Additionally, probate is also the formal testing and proving of the lack of a will, which allows the State to control the disposition of your property. There are so many reasons you want to avoid probate here are the main ones:

Probate takes a very, very long time.

Probate is full of fun and archaic names for things. This is but one of the reasons probate is very frustrating. For example, the words “testate” and “intestate” are really important for probate. The words “executor” and “administrator” are related and equally important. If you die “testate” it means that you died with a Will (or a poorly drafted trust). After your death, a court must verify your Will and appoint someone to be in charge of your estate. The person appointed by the court is called the “executor.”

By contrast, if you die “intestate” it means you died without any estate planning. After you die the court gets to decide what happens to your property. But before it makes any decisions it appoints a person to be in charge of the estate. The person appointed by the court to be in charge of the estate is called an “administrator.” Both the executor and administrator of an estate are referred to as the “personal representative” of the estate.

Starting the probate process.

Now that the words used in probate are a little more clear, let me explain the probate process.

Whether you have died with no plan or with a Will, the process is basically the same. In California, whether you have died testate or intestate, the process begins the same way. To start probate, someone needs to file a document with the probate court called a “Petition for Probate.” This document requests the probate court to appoint a personal representative to act on the estate’s behalf. The personal representative is the executor/administrator who pays all bills of the estate and communicates with the heirs, beneficiaries, and other relatives of the estate.

If a Petition for Probate is granted, the court gives the executor/administrator authority to officially administer the estate. This authorization given by the probate court to the executor/administrator is called “Letters of Administration.”

A typical probate will last for more than a year and some span several years. During this time, no one can take advantage of the estate property and the entire estate is being held up by the court.

What happens after the probate court appoints a personal representative

Once the probate court issues the Letters, the executor/administrator must complete an entire inventory of everything the deceased person owned. The inventory includes things like clothing, cars, real property, furniture, cash, stocks, investment accounts, retirement accounts, insurance proceeds, etc. The executor or administrator then submits a formal inventory to the court and to a court-appointed appraiser. The appraiser then officially appraises all of the property of the estate.

Additionally, the executor/administrator must give mandatory notices to all of the creditors or potential creditors of the estate. These notices allow the creditors and the various State entities to make claims against the estate.

Once all of the claims have been paid, settled, or litigated, the executor/ administrator files a final accounting with the court. The final accounting tells the court what estate property is left after all the bills and claims are paid. Once the final accounting is approved, the probate court orders the executor/administrator to distribute the estate property.

Where does the estate property go?

If the person died with a Will then the probate court will typically order the executor to distribute the estate according to the terms of the Will. But the probate court can ignore the language of the Will if someone challenges the terms of the Will, or if Will’s terms are illegal.

By contrast, if the person died with no plan, then the court will decide where the estate property goes. The California Probate Code specifies where the property goes through a formula known as “intestate succession.”

After the executor or administrator distributes the estate property, he or she must file receipts with the probate court. After the administrator/executor files the receipts with the court, he or she can file a document called an “Ex Parte Petition for Discharge.” This is the official document that releases the executor/administrator from all of his or her duties and formally closes the probate proceeding.

As the above summaries indicate, the probate process is exceedingly lengthy. Typical probate will last for more than a year and some span several years. During this time, the court prevents anyone from distributing the estate property.

Probate is very expensive and can costs thousands more than compared to other estate planning options

The California Probate Code says that both the executor/administrator and the attorneys are entitled to a percentage of the estate’s gross value. This is known as “statutory probate fees.”

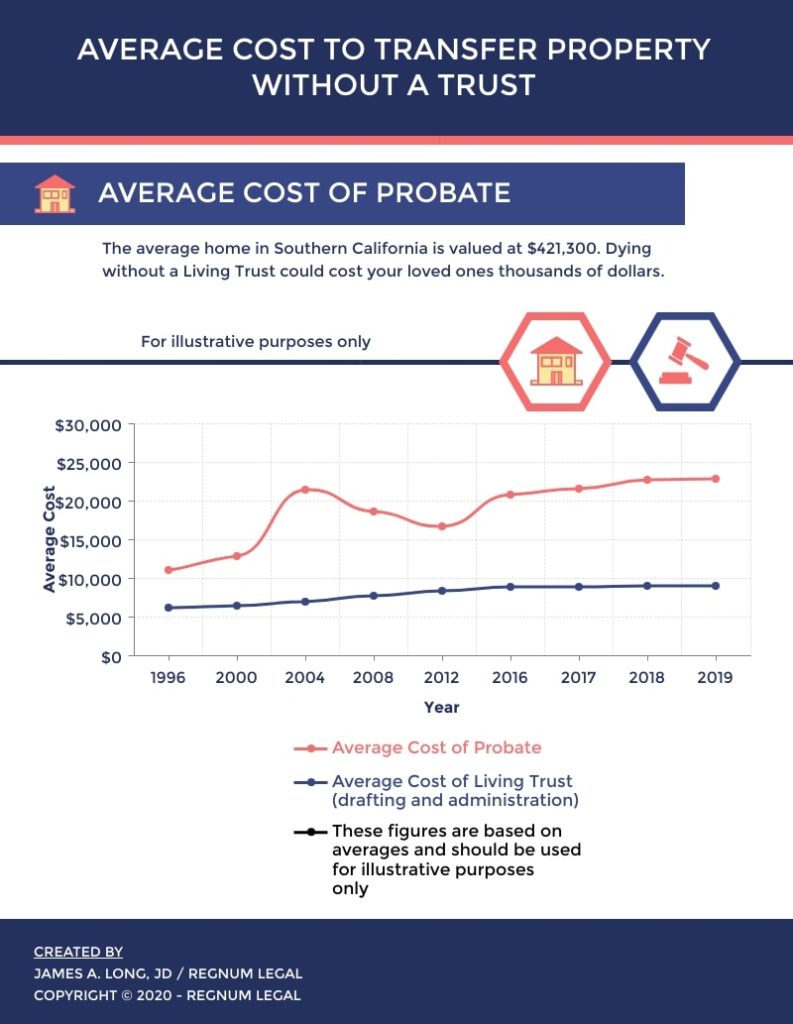

. . . the average cost of probate is over $22,000 . . .

To demonstrate why probate is so expensive, consider the following example:

In Southern California, the average home price is $421,300. Based on that number, the average cost of probate is over $22,000. So, if you own any real estate, especially in California, you should create a living trust to help your children avoid paying high fees just to inherit your family home.

In addition to the statutory probate fees, the court may award the attorney and the executor/administrator additional fees. The probate court usually awards extraordinary fees if some kind of objection or formal challenge is filed, which takes additional work.

Probate can be very frustrating.

The Probate Code strictly governs the entire probate process. These rules are so strict that being even one minute late on a required notice can delay or continue the probate process for months.

Additionally, family members or heirs have an almost unfettered right to file objections. Creditors can also object if their claims are not paid. As you can imagine, these types of objections only further delay the probate proceedings.

Finally, probate accounting is complex, detailed, and are highly scrutinized by the court. Improper accounting and simple mathematical errors often delay distribution for months.

Avoiding Estate Taxes

Effective estate planning helps you minimize the inheritance tax your children will pay upon your death. As of 2021, the current estate tax exemption is $11,700,000 per person, or $23,400,000 per married couple. The current estate tax rate is 40%. That means that your children will pay $0.40 for every dollar over $11,700,000 (or $23,400,000 if you’re married). But there is a catch. In order to get that extra exemption for a married couple you need to complete the lifetime exemption ($11,700,000) during your lifetime. Proper estate planning allows you to defer this gift even after the death of the first spouse, and can also allow your spouse to defer any estate tax until his or her death. Additionally, a revocable trusts and/or an irrevocable trusts can extend your tax savings even further.

But I do not have an estate over $11,700,000, you say. Well, you should know that the $11,700,000 estate tax exemption decreases automatically at the end of 2025 to under $6,000,000. Additionally, proposed legislation out of Congress indicates that the exemption may fall to $3,500,000. The estate tax exemption is not a constant. Not too long ago it was only $600,000. It changes almost as frequently as control of the U.S. House of Representatives. Even if you are not super wealthy, a good estate plan will allow your family at least some minimal tax planning in the event the tax laws change (or your assets increase).

Estate Planning Does Not Have to Be Expensive: A Living Trust Can Save You Thousands

With some proper estate planning, you will not need to go through the probate process. The third kind of plan for your estate on your death is a living trust. A living trust is a formal legal document that the law treats as a separate, distinct person (an alter ego). It operates much like a Will in that you get to decide who your beneficiaries are and where your property goes.

When you create a trust, the trust becomes a legal person capable of buying, selling, and owning property. Therefore, if you properly transfer all of your property to the trust prior to death, it avoids probate because, at the time of your death, you do not own any property – your trust owns it. Accordingly, the law acts as if you did not own the property and does not require the court to get involved. This has the added benefit of your entire plan remaining private. By contrast, a probate proceeding is always public record. If you already have a trust, or are considering creating your own trust on LegalZoom or Rocket Lawyer, you must seek proper legal advice to ensure that your trust is properly funded.

Be cautious, not all trusts are equal.

But a Living Trust is not without its own unique complexities. If you do not properly fund a trust, it is no better than a fancy Will. Even fancy Wills have to go through the probate process. I have represented numerous families whose loved ones died with an improperly funded trust. In these cases, I battled through lengthy probate proceedings to accomplish what should have been done during life.

Trust funding can be a complicated and detailed process. That’s why, if you already have a trust you must make sure it is funded. If you are considering creating your own trust online, it is imperative that you speak with a lawyer to help you fund the trust.

Another common estate planning problem when creating a trust is using ambiguous language. The person you pick to be in charge of your trust cannot understand what he or she is supposed to do if the trust is ambiguous. At that point, the probate court usually gets involved to provide authoritative instruction regarding the language of the trust.

Therefore, crafting a trust that is unambiguous and properly funded is essential. Preserving your legacy for the next generation demands proper estate planning.

Hallmarks of Good Estate Planning

Good estate planning means you have focused more on the “planning” and less on the documents that make up the estate plan. Having an “estate plan” is not the same as engaging in “estate planning.” Websites like LegalZoom and Rocket Lawyer give you access to living trust forms and estate planning documents, but do not actually help you “plan” your estate. In fact, there are even some “discount” living trust lawyers you can find who are no better than going to LegalZoom. Unless you engage with an experienced estate planning attorney you likely have engaged in minimal “estate planning” and your children are at risk of lawsuits, high taxes, expensive probate fees, and lengthy court battles.

Good estate planning not only provides you with a set of documents that clearly describe who gets your estate when you die, but also:

- Sets conditions upon how and when your young children can receive their inheritance.

- Avoids litigation through proactive follow-up with the estate planning lawyer.

- Reduces the tax your children may pay by appropriately holding your assets in one or more irrevocable trusts or a revocable living trust with special provisions upon death.

- Ensures that your minor children are cared for by the people you trust the most, AND NOT whoever the court appoints.

- Appropriately defines a succession plan for your business interests.

- Clearly articulates the medical decisions you do and do not want through a living wills or health care directives.

- Identifies an appropriate person to make financial decisions for you and (if necessary) your minor children in the event of your incapacity.

- Coordinates the distribution of your life insurance, retirement accounts, and any IRA / ROTH IRA you own.

- Provides an appropriate level of asset protection for your surviving spouse and children.

- Helps accomplish your charitable giving goals through one or more stand-alone charitable trusts or a charitable remainder trust.

- Includes appropriate provisions to help your beneficiary avoid gift tax.

- Names a contingent beneficiary to inherit your assets in the event your children do not survive you.

As you can see, estate planning is supposed to be comprehensive and thoughtful. Moreover, there are so many other considerations. If you own any real estate in California, you need a revocable trust, which will help you avoid probate, minimize taxes, and can provide some asset protection. If you are a business owner, you should also ask your estate planning attorney about business succession planning to ensure that your business is able to continue immediately after you pass. If you have a life insurance policy, you need to be sure to update your beneficiary designation to ensure that when the life insurance policy pays out, it does not conflict with your estate planning goals.

At Regnum Legacy, we are estate planning professionals and can help you with any of your estate planning needs. Call us for a free consultation (951) 228-9979.